Table of Contents

- In This Article

- Why the Confusion Exists

- What a Property Inspection Is

- What it includes

- What it doesn’t include

- What a Property Condition Assessment Is

- What it includes

- What it doesn’t include (without additional scope)

- Side-by-Side Comparison

- Which One Do You Need?

- The Gray Area: Multifamily

- What to Ask Before You Hire

- The Short Version

- Additional Resources

- Related Articles

- Contact

In This Article

- Why the Confusion Exists

- What a Property Inspection Is

- What a Property Condition Assessment Is

- Side-by-Side Comparison

- Which One Do You Need?

- The Gray Area: Multifamily

- What to Ask Before You Hire

Why the Confusion Exists

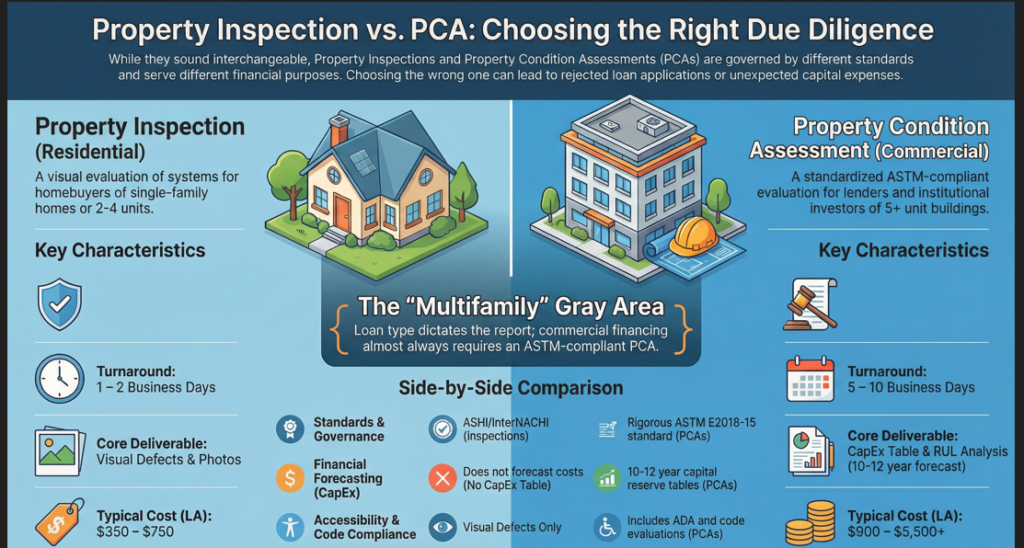

If you are buying property in Los Angeles and someone tells you to “get an inspection,” that could mean very different things depending on what you are buying. A property inspection on a single-family home and a property condition assessment on a 40-unit apartment complex are not the same service. They follow different standards, produce different deliverables, cost different amounts, and answer different questions.

The problem is that they sound interchangeable. People use “inspection,” “assessment,” and “condition report” loosely, and if you are moving from residential investing into commercial or larger multifamily deals for the first time, nobody explains when you have crossed the line from one to the other. The result is buyers who order the wrong service for their transaction , either overpaying for a report they don’t need, or underpaying for one that won’t satisfy their lender, insurer, or partners.

What a Property Inspection Is

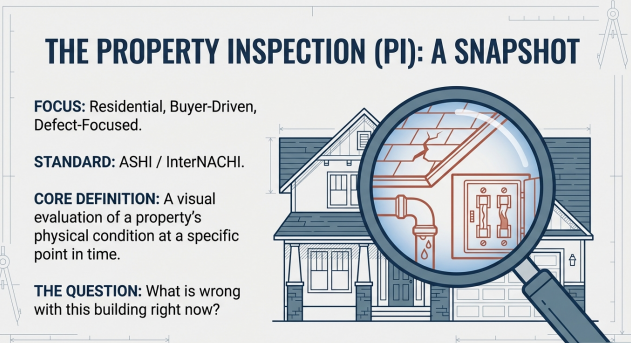

A property inspection—often called a home inspection—is a visual evaluation of a property’s physical condition at a point in time. In California, home inspections are performed according to Standards of Practice established by organizations like ASHI (American Society of Home Inspectors) or InterNACHI (International Association of Certified Home Inspectors).

The scope covers the major systems of a building: structure, roof, exterior, electrical, plumbing, HVAC, interior, insulation, ventilation, and fireplaces. The inspector identifies defects, safety concerns, and items that are not functioning as intended. The report tells you what is wrong, what needs attention, and what you should be aware of.

A property inspection is typically used for residential real estate transactions—single-family homes, condos, townhomes, and smaller multifamily buildings (2–4 units). It’s buyer-driven, performed during the inspection contingency period, and the report is written for a homebuyer audience. The format is descriptive: photos, observations, and recommendations organized by system or area.

What it includes

- Visual assessment of all major building systems

- Identification of defects and safety hazards

- Photo documentation (typically 100–300+ photos)

- Narrative descriptions of findings

- Recommendations for repair or further evaluation

What it doesn’t include

- Cost estimates for repairs

- Remaining useful life projections for components

- Capital expenditure forecasting

- Code compliance analysis (unless specifically added)

- Environmental assessments

What a Property Condition Assessment Is

A Property Condition Assessment (PCA) is a standardized evaluation of a commercial or large multifamily property performed in accordance with ASTM E2018-15 (or its most current edition). It’s an entirely different product from a home inspection, built for an entirely different purpose.

The ASTM standard defines the scope, methodology, and reporting requirements. A PCA evaluates the same physical systems a property inspection does—structure, envelope, roof, mechanical, electrical, plumbing—but it goes significantly further. The assessment includes remaining useful life estimates for every major component, a capital reserve table projecting replacement costs over a defined period (typically 10–12 years), and identification of code compliance issues, ADA accessibility concerns, and environmental conditions.

The report is written for an institutional audience: lenders, investors, asset managers, and their attorneys. It’s the document that goes into the due diligence file alongside the Phase I environmental assessment, the title report, and the rent roll analysis. Lenders frequently require a PCA for commercial and multifamily financing, and the report must conform to the ASTM standard to be accepted.

What it includes

- Physical condition assessment of all building systems

- Remaining Useful Life (RUL) analysis for major components

- Capital Reserve Table with projected costs over 10–12 years

- Immediate Repair Costs (deferred maintenance items)

- Short-Term Costs (items needing attention within 1–2 years)

- ADA accessibility evaluation

- Building code and fire code compliance observations

- Environmental screening (visible mold, asbestos-suspect materials, lead paint indicators)

- Site improvements assessment (parking, drainage, landscaping, paving)

- Document review (provided maintenance records, prior reports, permits)

- Executive summary for quick reference by decision-makers

What it doesn’t include (without additional scope)

- Phase I or Phase II environmental site assessments (separate ASTM standards)

- Seismic risk evaluation (often a separate PML study)

- Destructive or invasive testing

- Unit-by-unit interior inspection of every unit (unless specified, typically a representative sample is inspected)

Side-by-Side Comparison

| Property Inspection | Property Condition Assessment | |

| Standard | ASHI / InterNACHI Standards of Practice | ASTM E2018-15 |

| Typical Property | Single-family, condo, 2–4 unit | Commercial, 5+ unit multifamily, mixed-use |

| Audience | Homebuyer | Lender, investor, asset manager |

| Report Length | 40–80 pages | 100–200+ pages |

| CapEx Forecast | No | Yes (10–12 year projection) |

| Cost Estimates | Generally no | Yes (immediate, short-term, long-term) |

| ADA Evaluation | No | Yes |

| Code Compliance | Not standard (can be added) | Included |

| Lender Accepted | For residential mortgages | Required for most commercial loans |

| Typical Price (LA) | $350–$750 | $900–$5,500+ |

| Turnaround | Same day to next day | 5–10 business days |

Which One Do You Need?

You Need a Property Inspection If:

- You’re buying a single-family home, condo, or townhome

- You’re buying a small multifamily property (2–4 units) with conventional residential financing

- You’re a homeowner who wants a maintenance assessment

- You’re a seller preparing for listing (pre-listing inspection)

- Your lender has not specifically required an ASTM-compliant report

You Need a Property Condition Assessment If:

- You’re buying a commercial property (retail, office, industrial, mixed-use)

- You’re buying a larger multifamily property (5+ units) with commercial financing

- Your lender requires an ASTM E2018-compliant report

- You’re an institutional investor or fund with due diligence standards

- You need CapEx projections for underwriting

- You need ADA compliance evaluation

- The report will be reviewed by attorneys, lenders, or insurance underwriters

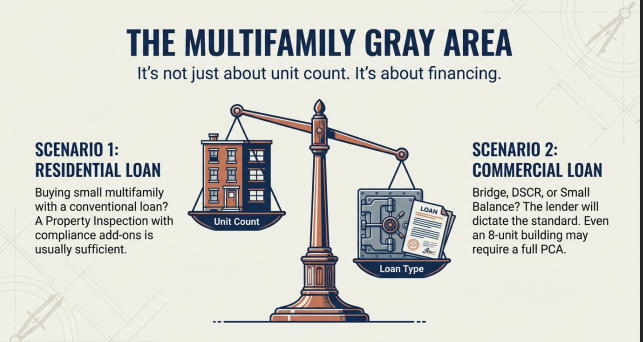

The Gray Area: Multifamily

The place where this gets complicated is multifamily. A duplex clearly needs a property inspection. A 50-unit apartment complex clearly needs a PCA. But what about a 6-unit building? An 8-unit? A 12-unit?

The answer depends less on the unit count and more on the financing and the buyer’s needs.

If you are buying a small multifamily building with a residential loan, a property inspection with compliance add-ons (permit research, RHHP status, SB 721 check) may be sufficient. It gives you the physical condition, and the add-ons catch the LA-specific regulatory issues.

If you are buying with commercial financing ,a bridge loan, a DSCR loan, a Freddie Mac Small Balance Loan, or similar—the lender almost certainly requires a PCA. It doesn’t matter that the building only has 8 units. The loan product dictates the report standard.

And if you are an investor who needs to underwrite the deal with CapEx projections and present the due diligence package to partners, a PCA gives you the financial framework that a standard inspection doesn’t. The capital reserve table alone can justify the additional cost because it tells you what you will need to spend, and when, over the next decade.

For LA multifamily specifically, regardless of which report you order, make sure the scope includes RHHP compliance status (for unincorporated areas), SB 721 balcony inspection status (for 3+ units), and permit history research. These are LA-specific compliance issues that neither a standard home inspection nor a standard ASTM PCA automatically covers, but they directly affect your operating costs and legal exposure from day one.

What to Ask Before You Hire

Not every inspector offers both services. And not every inspector who claims to do PCAs actually follows the ASTM standard. Before you hire, ask:

- What standard do you follow? For a PCA, the answer should be ASTM E2018-15 (or the current edition). If they can’t name the standard, they are not doing a PCA.

- Will the report include a capital reserve table? This is a core PCA deliverable. If there is no CapEx projection, it is not an ASTM-compliant assessment.

- Will the report satisfy my lender? Ask your lender what they require before you engage an inspector. Getting the wrong report wastes time and money.

- Do you have commercial inspection credentials? Look for ASHI Commercial certification, InterNACHI Commercial training, ICC certification, or equivalent. An architecture or engineering background is a strong indicator of someone who understands building systems at the commercial level.

- Can you add compliance scope for LA-specific requirements? RHHP, SB 721, permit research, and RSO status are not part of either a standard home inspection or a standard ASTM PCA. They need to be specifically scoped.

The Short Version

A property inspection tells you what is wrong with a building. A property condition assessment tells you what is wrong, what it will cost, when things will need replacement, and whether the building meets the standards your lender and partners require. Both are valuable , but they are different tools for different jobs, and using the wrong one for your transaction creates gaps that cost money to fill later.

If you are not sure which service fits your situation, I am happy to talk it through. There’s no cost for a phone call, and I would rather help you order the right report the first time than sell you one that doesn’t serve your needs.

NS

Additional Resources

Related Articles

Contact

- Phone: (626) 214-5929

- Email: nathan@larentalinspections.com

Get Ahead of Your Inspection

Book an inspection today and get ahead of your inspection. We'll help you get the most out of your inspection.

Schedule InspectionQuestions?

Email: nathan@larentalinspections.com

Call/Text: (626) 214-5929

Serving all of Los Angeles County